Determining a new recruit’s employment status is a critical task for employers, as this decision carries significant legal and tax implications. Understanding IR35 rules is essential in this process. Businesses must decide early on in the recruitment process whether an individual should be treated as an ‘employee’, a ‘worker’ or a ‘self-employed person’ (independent contractor). Each category holds different benefits and obligations for both the employee and the individual; employers should be well-versed in these differences to come to a decision which accurately reflects that person’s working arrangement.

The intricacies of these arrangements are reflected in the contracts used by employers, and this article will contrast the use of zero-hour contracts and regular employment contracts which usually determine whether an individual is classed as a ‘worker’ or an ‘employee’. We will also discuss the importance of the IR35 legislation, often referred to as the ‘off-payroll working regime’, which ensures that despite the formal representation of an individual’s status as a ‘worker’, they may still be subject to PAYE tax and National Insurance contributions like any other employee. The wrong decision may lead to employment tribunal claims or tax penalties; however, new changes coming into force on 6th April 2024 will reduce any unfair burden on employers and individuals who have overpaid their tax in error.

The Employment Rights Bill (ERB) proposes reforms that may alter employment status definitions and expand worker protections in the future, but these changes are not yet legally in force. Current obligations under existing law remain in effect.

Understanding the differences between zero-hour contracts and standard employment contracts

Zero-hour contracts may get a bad rap in discussions about the ‘gig economy’ and underemployment, but they are rising in popularity as a flexible tool for employers and workers alike. The Chartered Institute of Personnel and Development (CIPD) define zero-hour contracts as ‘working arrangements where there is no guaranteed number of hours that must be worked (or paid for).The contract will provide for that individual’s remuneration and the terms under which work may be offered or turned down. As the worker is not obliged to work a particular number of hours, this means that the employer can offer the worker zero hours in any one week without breach of contract. This arrangement allows flexibility for the employer to respond to fluctuations in demand and flexibility for individual workers to determine their workload, which explains why 14-16% of small and medium-sized businesses utilise zero-hour contracts (according to a survey in 2021). In addition, the number of people on zero-hour contracts in the UK is rising year-on-year, from approximately 1.03 million in 2022 to 1.18 million in 2023.

In line with these reduced obligations on the part of the ‘worker’, they are afforded less protection and rights under employment law. For example, key employment rights such as the right to maternity leave and redundancy pay are only given to those deemed ‘employees’, whilst ‘workers’ are given other rights such as entitlement to holiday and holiday pay, and auto-enrolment in pension schemes. This serves as a hierarchy, in that all employees are also workers, but not all workers are employees. Zero-hour workers are also given specific protection from ‘exclusivity clauses’, which attempt to prohibit that worker from doing other work without the employer’s consent. Such clauses are deemed ‘unenforceable’, and any breach of this term would not count as a fair ground for dismissal.

Employee or worker?

An employee is defined in the Employee Rights Act 1996 as ‘an individual who has entered into or works under a “contract of employment”’. This contract may be express or implied and may be oral or in writing. There are several other criteria to determine whether an individual is an employee, but most importantly, there must be ‘mutuality of obligation’ between the employee and their employer, a phrase which has been debated in the courts. This difference is what distinguishes the ‘worker’ from the ‘employee’, as for workers, there is no obligation to take on a specific amount of work in any one week, and similarly, there is no obligation for employers to offer them an amount of work in any one week. There must also be ‘continuity of employment’, that is, a level of regularity to the work, which is offered and accepted from week to week.

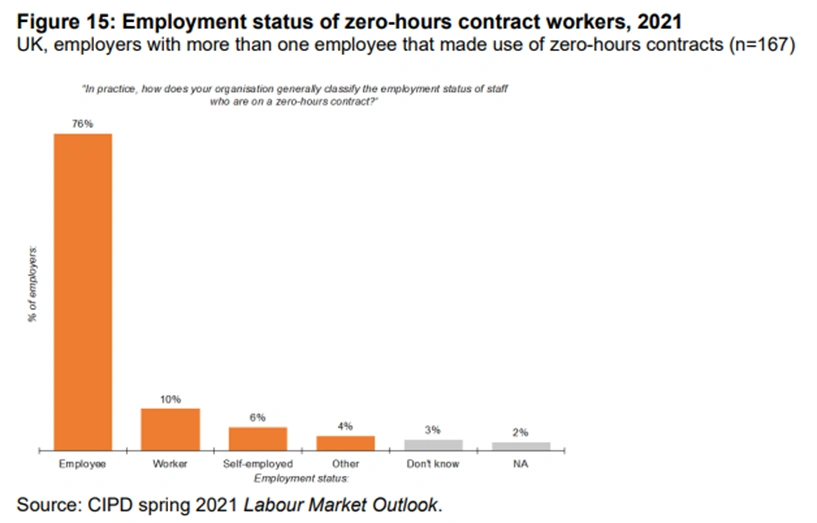

However, this does mean that some individuals working under zero-hour contracts are, in fact, deemed to be ‘employees’, if in reality there is both mutuality of obligation and ‘continuity of employment’. The employment tribunal or the tax office has the final say about whether the individual is an employee or a worker based on their individual circumstances, and these facts will take precedence over any written contract or oral agreement. According to a CIPD survey, 76% of zero-hour contract workers were given ‘employee’ status.

The ERB may eventually introduce additional protections for zero-hour contract workers, but these are not yet legally in force.

How are zero-hours contracts affected by IR35?

The IR35 is an important piece of tax legislation which is aimed at people who work for a company through an intermediary, such as an agency, a personal service company or a partnership, but still do similar work to formal employees. Many of these intermediaries choose to use zero-hour contracts to respond to short-term staffing needs or fluctuating demand. The IR35, or the ‘small-client off-payroll working regime’, ensures that these so-called ‘disguised employees’ pay roughly the same amount of income tax and National Insurance contributions as formal employees. The responsibility for deciding whether an individual falls within IR35 (is defined as an employee despite working for an intermediary), falls on the employer, so it is crucial to examine thoroughly whether the IR35 applies.

The IR35 regime will apply if the worker is not bound by a contract with the ‘end client’, as they are working under an intermediary, but they are nevertheless obliged to provide services for that end client and would be regarded as an employee if they did have a contract. This is called the ‘notional’ or ‘hypothetical’ contract. The HMRC has provided the Check Employment Status for Tax (CEST) tool to cut down on confusion. If there is an error, the employer will face employment tribunal claims or tax penalties. Currently, if the employer fails to determine that an individual falls under the IR35 regime, the HMRC is not under any duty to reduce the tax liability of the employer to reflect income tax already paid by that worker or the intermediary company. From the 6th April 2024, it is formally required that the HMRC take previous taxes paid by the worker or the intermediary into account before penalising the employer, which will avoid double payment of tax and reduce any unfair burden on the employer.

Conclusion

To conclude, determining employee status and compliance with the IR35 regime is a tricky area of law for employers to navigate, with significant consequences for errors, despite the changes coming into force on 6th April. The CEST tool is useful in this regard – a new CEST 2.0 has recently been released in October 2023 to improve its functionality. And whilst zero-hour contracts are useful to increase flexibility, employers should carefully consider the circumstances of each individual working arrangement, as this is considered the most important by the employment tribunal and may override any formal contractual agreement.

Reading:

CIPD Spring 2021, Labour Market Outlook (CIPD Report, ‘Zero-Hours Contracts: Evolution and Current Status’, 2022)

{kind=link}

Farringford Legal is your growth partner, providing affordable, expert legal services across England & Wales with a client-centric, entrepreneurial approach. We are not just lawyers; we are allies in your business journey, adapting as your business evolves, deeply trustworthy, always responsive.

www.farringfordlegal.co.uk | info@farringfordlegal.co.uk